Credit cards have become an essential part of our financial lives, providing us with a convenient and flexible means of making purchases. However, it’s crucial to understand the financial implications associated with credit card usage. One significant aspect that plays a crucial role in managing credit card debt is the APR, or Annual Percentage Rate. In this article, we will explore what is a good APR for a credit card is and how it affects your financial decisions.

Understanding APR

Definition of what is a good APR for a credit card

APR, or Annual Percentage Rate, is the annualized cost of borrowing money and is expressed as a percentage. It takes into account the interest charged by the credit card issuer and any other applicable fees. What is a good apr for a credit card provides a standardized way of comparing credit card offers, allowing consumers to evaluate the cost of credit across different cards.

Importance of APR in Credit Cards

The APR on a credit card significantly impacts the overall cost of carrying a balance. A higher APR means paying more in interest charges, making it important to choose credit cards with lower interest rates. Understanding the factors that influence credit card APR can help you make smarter decisions when selecting a credit card.

Factors Influencing Credit Card APR

Credit Score

One of the primary factors that determine your credit card APR is your credit score. Higher credit scores usually result in lower APRs, as they indicate a history of responsible borrowing and repayment.

Credit Card Type

Different types of credit cards come with varying APR ranges. For example, rewards cards often have higher APRs than basic cards without rewards. It’s essential to consider the features and benefits of a credit card in relation to its APR to make an informed choice.

Average APR Range for Credit Cards

Credit card APRs can vary significantly based on various factors. Here’s a breakdown of the average APR range for credit cards:

Low APR Credit Cards

Low APR credit cards generally have APRs in the range of 10% to 15%. These cards are suitable for individuals who tend to carry balances or expect to finance larger purchases over time. They provide a more affordable option for interest payments compared to cards with higher APRs.

High APR Credit Cards

High APR credit cards have APRs that exceed 20%. These cards are often geared towards individuals with lower credit scores or those who prioritize other card features over the interest rate. It’s important to exercise caution when using high APR credit cards to avoid excessive interest charges.

Strategies to Obtain a Lower APR

While credit card issuers determine the APR you receive, there are strategies you can employ to obtain a lower APR:

Improving Credit Score

Working on improving your credit score can help you qualify for credit cards with lower APRs. By paying bills on time, reducing debt, and maintaining a healthy credit utilization ratio, you can enhance your creditworthiness and potentially secure better APRs.

Transferring Balances to Lower APR Cards

Another strategy to consider is transferring balances from high APR cards to ones with lower rates. Many credit card issuers offer promotional balance transfer offers with 0% or low introductory APRs. This can help you save on interest charges and pay down your debt faster.

The Impact of APR on Card Debt

Compound Interest and Long-term Debt

Credit card debt can quickly accumulate due to compound interest. High APRs can significantly increase the cost of carrying a balance, making it challenging to pay off debts. It’s important to understand the long-term impact of high APRs and prioritize paying off higher interest debt first.

APR and Introductory Offers

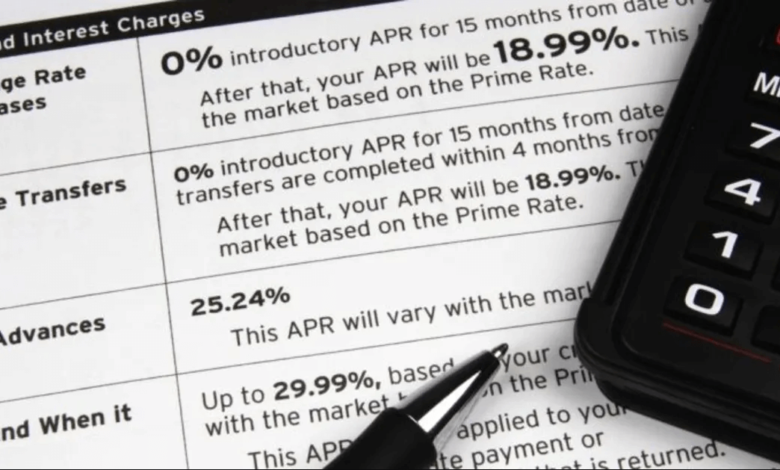

0% APR Introductory Periods

Some credit cards offer 0% APR introductory periods, typically ranging from 6 to 18 months. During this period, you won’t accrue interest on new purchases or balance transfers. However, it’s essential to review the terms and conditions of these offers, as they may have specific requirements or revert to higher APRs once the introductory period ends.

Cash Back and Rewards Cards

Cash back and rewards cards often come with higher APRs due to the additional benefits they offer. While the APR is important, it’s crucial to consider the rewards and cash back opportunities provided by these cards. If you can pay your balance in full each month, the rewards can outweigh the higher APR.

How to Compare Card APR

When comparing credit cards, it’s essential to consider the APR along with other factors:

Annual Fee Considerations

Some credit cards charge an annual fee in exchange for benefits or rewards. When assessing the APR, it’s important to factor in any annual fees associated with the card to determine the overall cost of credit. Read more…

Conclusion

The APR of a card is a critical factor to consider when managing your finances and choosing the right credit card for your needs. By understanding what an average APR for a credit card is and how it impacts your overall debt, you can make informed decisions that align with your financial goals. Remember to compare different credit card options, consider your credit score, and explore strategies to obtain lower APRs for a more favorable financial future.

FAQs

FAQ 1: What is a good APR for a credit card?

A good APR for a credit card is typically considered to be below 15%. However, the specific APR that is considered good can vary depending on individual circumstances and creditworthiness. It’s always beneficial to aim for lower APRs to minimize interest costs.

FAQ 2: Can you negotiate your credit card APR?

Yes, in some cases, you can negotiate your credit card APR. It’s worth contacting your credit card issuer, especially if you have a good payment history or if you’ve received a pre-approved offer from another card issuer. Negotiating a lower APR can help you save on interest charges.